Building the industry for the 21st century with new solutions

In response to the demonstration for our industry that brought more than 10,000 people to Brussels in September, Pieter Timmermans, head of the FEB (Federation of Enterprises in Belgium), presented his vision for relaunching Belgium's industry. For him, cutting wages and eliminating the recognition of overtime is the way forward... In other words, the proposals emanating from the future Arizona government coalition (named after the U.S. State that has in its flag the five colors of the coalition’s composing parties). Harmful measures that have already proved ineffective.

While other countries are investing massively in research, infrastructure and technology to gain a strategic lead in key sectors such as electric vehicles and batteries, Pieter Timmermans is proposing a return to the past with "measures that have been in place in the rest of Europe for 80 years". As if the threat of de-industrialization is just a Belgian problem and not a Europe-wide issue...

Pieter Timmermans suggested taking "drastic measures" to combat the "wage handicap", which he sees as the main cause of the industry's current difficulties. In a similar vein, Stefaan Michielsen, editor of financial daily De Tijd, argues that the crisis in industry is "due to the increase in wage costs caused by automatic wage indexation". Parties such as N-VA (Flemish nationalist), CD&V (Christian-democrat), MR (neoliberal) and even Vlaams Belang (fascist) are all singing the same song, repeating that "wage costs" are responsible for the industrial crisis. Vlaams Belang goes so far as to declare that "the crucial point remains the wage cost and the competitiveness of our companies in the face of foreign competition. We shouldn't kid ourselves."

But today, the industrial problem in Europe and Belgium does not boil down to wage competitiveness, as Timmermans suggests. Germany, where real wages have fallen by 4% since 2020, is on the verge of a recession and faces a drop in industrial production. Geert Bruyneel, former CEO of Volvo Cars in Ghent, reminds us: "In Sweden, labour costs are also high. But in the final assembly stage, wage costs only account for 10%."

Europe's real industrial challenge lies elsewhere. As Mario Draghi, former president of the European Central Bank (ECB), pointed out in his report, we are facing an "existential challenge" for our European industry, which is both energetic and technological. Our high energy prices are holding back our industrial capacity, and we are lagging behind in terms of investment in research and development. The key to revitalizing industry in Europe lies in massive public and private investment, not in outdated solutions.

A paradigm shift to meet the energy challenge

High and volatile energy prices are one of the main threats to the industrial sector in Europe and Belgium. The utilization rate of production capacity in energy-intensive sectors such as chemicals is at historically low levels. The underlying cause of these high prices is the liberal character of the energy market. Even though we have never faced actual shortages, energy prices have been the subject of considerable speculation, stimulated by supply problems and geopolitical instability. Cheaper Russian gas has been replaced by more expensive shale gas from the United States. As Mario Draghi pointed out, gas prices in Europe are still four to five times higher than in the United States, and electricity prices two to three times higher.

Europe urgently needs to free itself from this energy dependency and from the market mechanisms that encourage speculation. When it comes to renewable energy production in Europe, the North Sea is our main asset. But the required investments are lagging behind, and there is no guarantee that current plans will actually be implemented. Inflation, supply problems and rising interest rates are making investment much more expensive and deter private investors. The prospective profits are not sufficiently secure or substantial to convince multinationals to make the investments needed.

Massive investment to make up for our technological lag

On the technological front, Europe is struggling to catch up with China and the United States, and Timmermans is not proposing any solutions to remedy this. As Koen Schoors, professor of economics at Ghent University, points out, as far as the automotive industry is concerned, Europe has delayed the transition to electric cars for too long, letting China take a technological lead of 10 to 15 years. Not only does China now excel in the production of electric cars, it also dominates the battery sector, a key industry for electrification. Faced with China's rapid development, the United States launched a vast subsidy program, the Inflation Reduction Act.

This aims to attract investment in forward-looking industrial sectors such as batteries, wind turbines and other technologies of the future. And Washington doesn't hesitate to contact our industry directly to lure it across the Atlantic. Meanwhile, the Volkswagen Group distributes 11 billion euros in dividends to its shareholders rather than reinvesting these resources in the industry of the future and making up for its technological lag.

For an ambitious plan

Revitalizing our industry does not mean cutting wages or relaxing labour standards, as Timmermans advocates. The boss of bosses should have more respect for those who keep industry running. What we need is:

1. A genuine Energy Plan that guarantees abundant and affordable energy in line with climate objectives. We can't afford to lag behind in the development of the renewable energy sector just because of the vagaries of the free market. If we want to anchor manufacturing and employment in Europe, we need public investment and public control of our energy. A genuine energy plan must also include a price control mechanism to avoid speculative excesses.

2. Ambitious investment in research and development. We need to invest massively in R&D, based on a vision for the future. The industry also needs to reinvest its profits in innovation, rather than handing out colossal dividends, so that we can position it for the technologies of tomorrow, rather than use the outdated recipes of the past.

The future of Belgian and European industry rests first and foremost on the energy transition and massive investment in research and development. The solutions proposed by Pieter Timmermans belong to a bygone era. To build the industry of the 21st century, we need innovative solutions, public and private investment, and policies that look resolutely to the future.

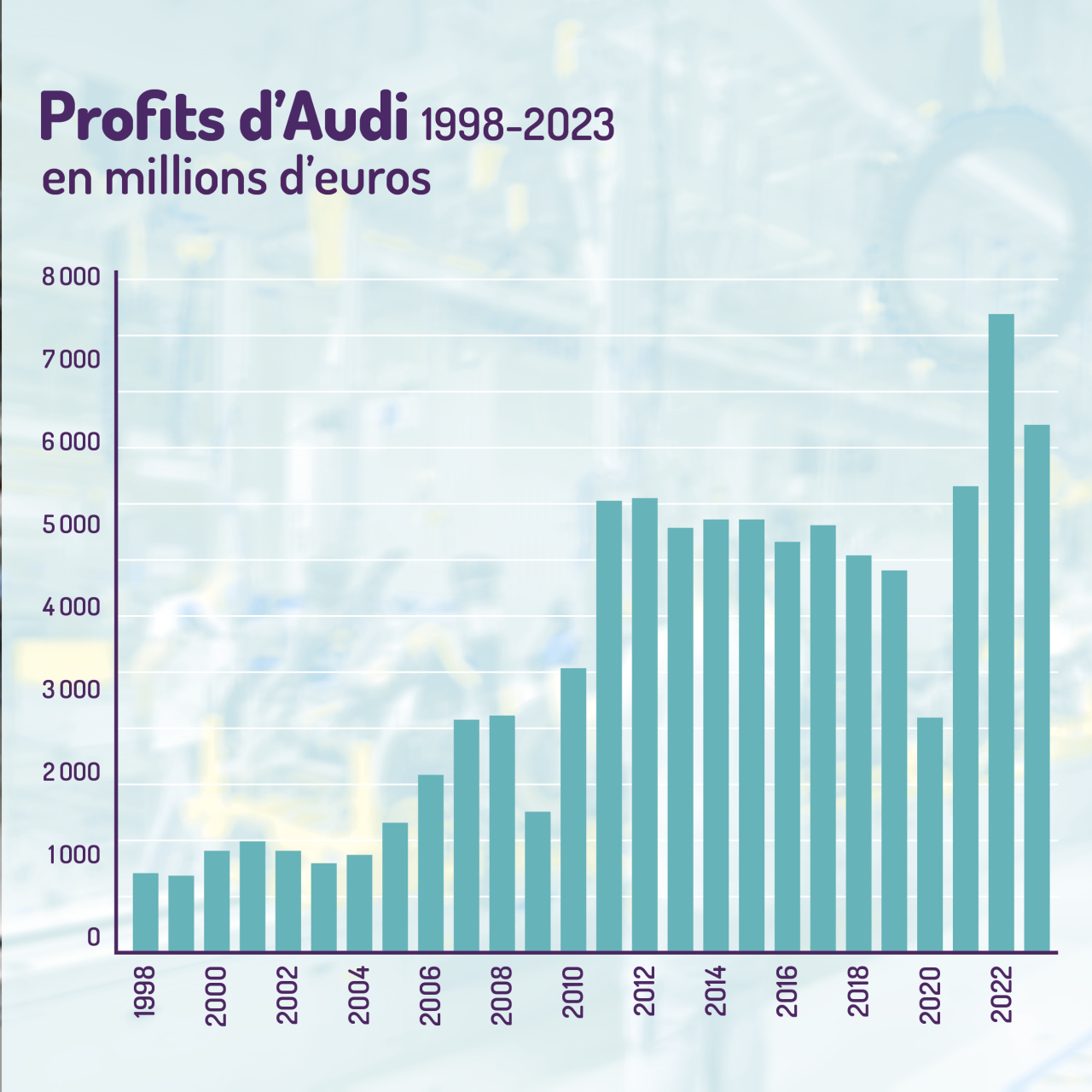

Historic profits for Audi and VW The Audi Group achieved its two biggest profit margins ever in 2022 and 2023, thanks to the hard work of its workers. In 1998, operating profit remained below the billion euro mark, whereas it reached 6.3 billion euros in 2023 and 7.6 billion in 2022.

This is why the financial newspaper LʼEcho has written that Audi "is a cash cow for the Volkswagen Group". The Volkswagen Group, Europe's biggest automaker, to which the Audi brand belongs, distributed almost 12 billion in dividends to its shareholders in 2023. It was a historic year for the Group's shareholders, who have grown exponentially richer over the last 25 years. So it's not because Audi or Volkswagen are experiencing financial difficulties that they plan to close the Forest plant next February. It's because they made strategic mistakes. And they are now threatening the jobs of 4,500 workers and the survival of an industrial flagship.

The governments of Belgium and Europe, for their part, are responsible for their total lack of an industrial strategy to ensure the technological and ecological transition. As a result, the European automaker is lagging far behind its competitors, and demand for electric cars has slowed sharply.

The Volkswagen Group has the means to ensure an industrial future for the Forest site. They can decide to protect jobs, the technological jewel that is the Forest plant, and the remarkable know-how that workers have accumulated through a million training hours. The PVDA-PTB demands a moratorium to prohibit the closure of automotive plants as long as there is no alternative - either another model or a buyer. We will mobilize to prevent Audi's management from selling up, making a lucrative financial deal and showering shareholders with even more cash.

They can also afford to pay very good bonuses to workers at Audi and at all its subcontractors. The PVDA-PTB has tabled a bill to ensure that subcontractors' workers will be guaranteed the same conditions as the workers at the parent plant. |